Covered Call (Buy/Write)

Description

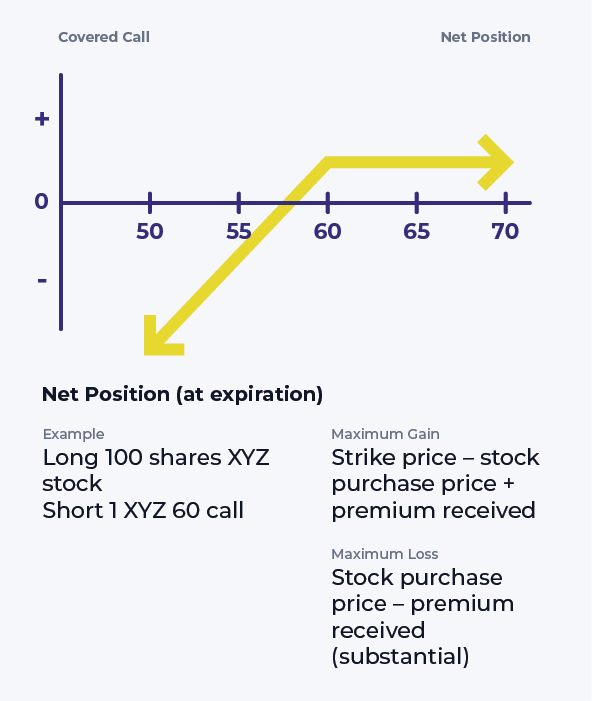

An investor who buys or owns stock and writes call options in the equivalent amount can earn premium income without taking on additional risk. The premium received adds to the investor’s bottom line regardless of the outcome. It offers a small downside ‘cushion’ in the event the stock slides downward and can boost returns on the upside.

Predictably, this benefit comes at a cost. For as long as the short call position is open, the investor forfeits much of the stock’s profit potential. If the stock price rallies above the call’s strike price, the stock is increasingly likely to be called away. Since the possibility of assignment is central to this strategy, it makes more sense for investors who view the assignment as a positive outcome.

Because covered call writers can select their own exit price (i.e., strike plus premium received), an assignment can be seen as a success; after all, the target price was realized. This strategy becomes a convenient tool in equity allocation management.

The investor doesn’t have to sell an at-the-money call. Choosing between strike prices simply involves a tradeoff between priorities.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.