Naked Call (Uncovered Call, Short Call)

Description

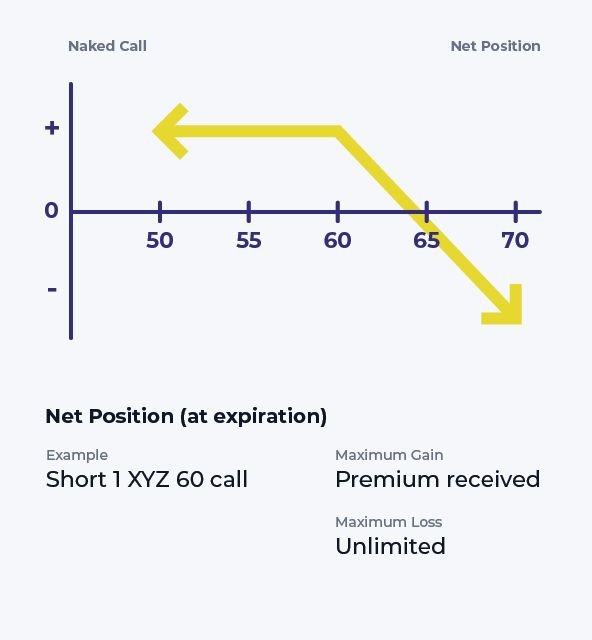

An investor who writes a call option without owning the underlying stock is banking on a flat to bearish short-term forecast for the stock. The strategy consists of writing the call in hopes that it will lose value through time decay and eventually expire out-of-the-money. If the term ends without the option being assigned, the writer keeps the entire premium initially received, and all obligations under the short call position terminate.

The strategy’s staggering risk stems from the investor’s obligations should the stock unexpectedly rally and the call be assigned. The naked call writer has no way to offset assignment risk. To make matters worse, the obligation is open-ended. Since there is no limit to how high the stock’s price could rise, there is no upper boundary to the losses to be incurred in acquiring the stock for delivery in the event of assignment. Choosing higher strike prices and shorter expiration terms could make the strategy somewhat less dangerous, but there is simply no way to predictably counter the huge risk.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.