Synthetic Short Stock

Description

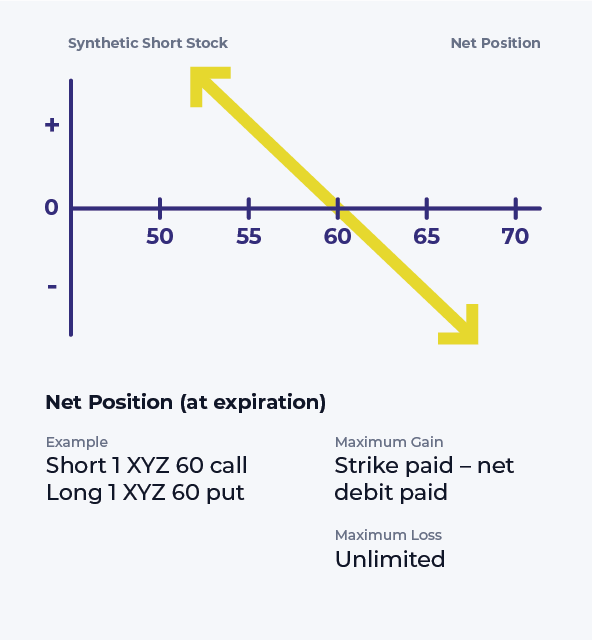

The strategy combines two option positions: short a call option and long a put option with the same strike and expiration. The net result simulates a comparable short stock position’s risk and reward. The principal differences are the time limitation imposed by the term of the options, the absence of the large initial cash inflow that a short sale would produce, and the absence of the practical difficulties and obligations associated with short sales.

If assigned, the investor who doesn’t take further steps to cover ends up with an actual short stock position.

Outlook

Looking for a decline in the stock’s price during the term of the options.

Since the strategy’s term is limited, the longer-term outlook for the stock isn’t as critical as for, say, an outright short stock position.

However, the difficulty of pinpointing the exact timing and sequence of a downturn, just before an upturn, suggests it is not an optimal strategy for a long-term bullish investor.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.

© 2024 Lightspeed Financial Services Group, LLC. All rights reserved.

Equities, equities options, and commodity futures products and services are offered by Lightspeed Financial Services Group LLC (Member FINRA, NFA and SIPC). Lightspeed Financial Services Group LLC’s SIPC coverage is available only for securities, and for cash held in connection with the purchase or sale of securities, in equities and equities options accounts. You may check the background of Lightspeed Financial Services Group LLC on FINRA’s BrokerCheck.

Options trading entails significant risk and is not appropriate for all investors. Certain complex options strategies carry additional risk. Before trading options, please read Characteristics and Risks of Standardized Options

ETFs are subject to market fluctuation and the risks of their underlying investments. ETFs are subject to management fees and other expenses.