Long Ratio Put Spread

Description

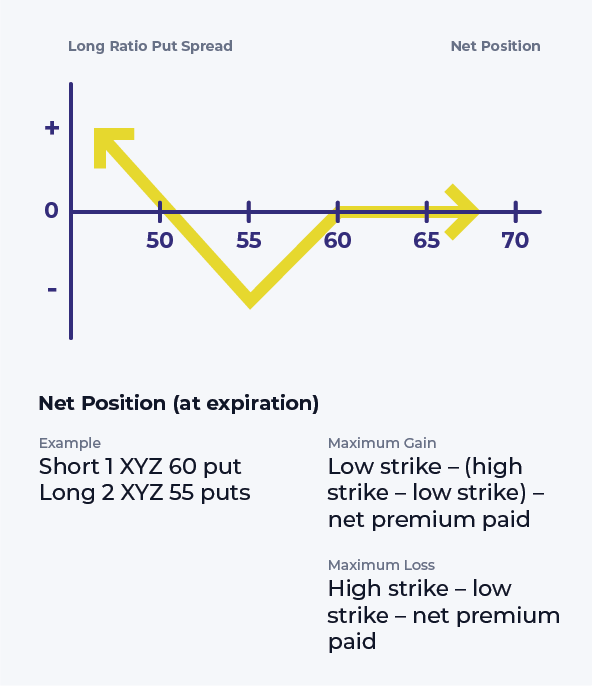

The long ratio put spread is a 1×2 spread combining one short put and two long puts with a lower strike. All options have the same expiration date. This strategy is the combination of a bull put spread and a long put, where the strike of the long put is equal to the lower strike of the bull put spread.

Outlook

The investor is looking for either a sharp move lower in the underlying stock or a sharp move higher in implied volatility during the life of the options.

Summary

The initial cost to initiate this strategy is rather low, and may even earn a credit, but the downside potential can be substantial. The basic concept is for the total Delta of the two long puts to roughly equal the Delta of the single short put. If the underlying stock only moves a little, the change in the value of the option position will be limited. But if the stock declines enough to where the total Delta of the two long puts approaches -200, the strategy acts like a short stock position.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.

© 2024 Lightspeed Financial Services Group, LLC. All rights reserved.

Equities, equities options, and commodity futures products and services are offered by Lightspeed Financial Services Group LLC (Member FINRA, NFA and SIPC). Lightspeed Financial Services Group LLC’s SIPC coverage is available only for securities, and for cash held in connection with the purchase or sale of securities, in equities and equities options accounts. You may check the background of Lightspeed Financial Services Group LLC on FINRA’s BrokerCheck.

Options trading entails significant risk and is not appropriate for all investors. Certain complex options strategies carry additional risk. Before trading options, please read Characteristics and Risks of Standardized Options

ETFs are subject to market fluctuation and the risks of their underlying investments. ETFs are subject to management fees and other expenses.