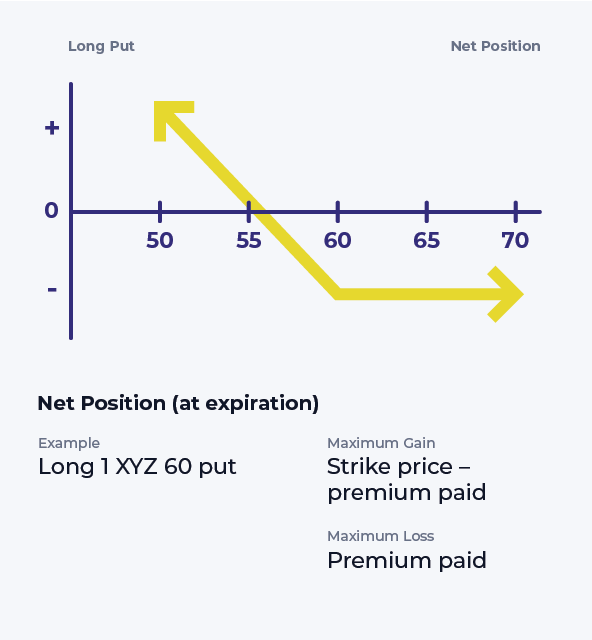

Long Put

Description

The investor buys a put contract that is compatible with the expected timing and size of a downturn. Although a put usually doesn’t appreciate $1 for every $1 that the stock declines, the percentage gains can be significant.

Exercising a put would result in the sale of the underlying stock. These comments focus on long puts as a standalone strategy, so exercising the option would result in a short stock position, something not all individuals would choose as a goal. The plan here is to resell the put at a profit before expiration. The investor is hoping for a dramatic downturn; the sooner, the better.

Timing is of the essence. Some put holders set price targets or re-evaluation dates; others ‘play it by ear.’ Either way, all value must be realized before the put expires. If the expected results have not materialized as expiration draws near, a careful investor is ready to re-evaluate.

If the put holder is willing to forfeit 100% of the premium paid and is convinced a decline is imminent, one choice is to wait until the last trading day. If the stock falls, the put might generate a nice profit after all. However, if a quick correction looks unlikely, it might make sense to sell the put while it still has some time value. A timely decision might recover part or even all of the investment.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.

© 2024 Lightspeed Financial Services Group, LLC. All rights reserved.

Equities, equities options, and commodity futures products and services are offered by Lightspeed Financial Services Group LLC (Member FINRA, NFA and SIPC). Lightspeed Financial Services Group LLC’s SIPC coverage is available only for securities, and for cash held in connection with the purchase or sale of securities, in equities and equities options accounts. You may check the background of Lightspeed Financial Services Group LLC on FINRA’s BrokerCheck.

Options trading entails significant risk and is not appropriate for all investors. Certain complex options strategies carry additional risk. Before trading options, please read Characteristics and Risks of Standardized Options

ETFs are subject to market fluctuation and the risks of their underlying investments. ETFs are subject to management fees and other expenses.